Hillbilly Elegy

Hillbilly Elegy, by J.D. Vance, has received a lot of attention recently. It is the story of a young man with Appalachian roots whose immediate family moved to Middletown, Ohio. The family was rife with domestic violence, divorce, drug abuse and stress. It was also full of love. Vance eventually succeeded beyond the wildest dreams of his “hillbilly” friends and family, graduating from Yale law school, landing a well-paying job, and having a loving stable marriage.

The book is a canvas upon which you can paint your own conclusions. The Wall Street Journal lauded it for demonstrating how folks can overcome social and economic liabilities through mentoring and a large dose of personal responsibility. Vance does attribute much of his success to his grandparents who guided and protected him. But he also acknowledges that government programs, such as Pell grants and low-interest student loans, were important. Vance says that while the social problems and destructive behaviors of the working class cannot be solved by government alone, government policies can act like a thumb on the scale in favor of the working poor.

But another force took over later. At Ohio State, where Vance attended as an undergraduate, and at Yale he was the beneficiary of connections. Connections helped him get into an Ivy League law school; connections helped him get interviewed and hired by a prestigious law firm. He realized that using connections is how the upper middle class and very wealthy routinely succeed. Lack of connections is a big reason why the poor and working class cannot flourish with the same regularity.

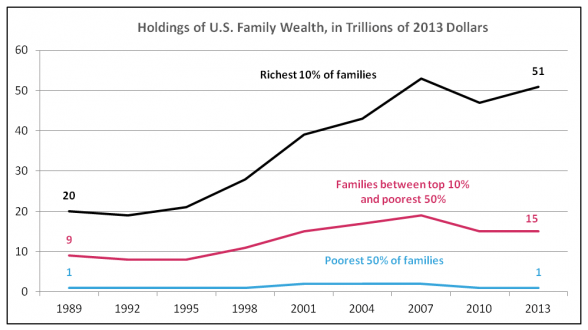

In the current debates about economic growth and tax policy, we often hear arguments that suggest a person’s economic status is a measure of his or her virtue. As Robert Reich put it in his book Reason, “If you’re rich you must somehow deserve it. If you’re poor, you deserve that, too.” But many of the super-wealthy inherited their wealth and added nothing to society to get it. Think Paris Hilton. More to Vance’s experience, Reich notes that the false connection between wealth and virtue fails to recognize that

the rich were lucky to be born into families that gave them access to excellent primary and secondary schools, talented teachers and tutors, summer “enrichment” programs, prestigious universities, and all the contacts and connections that come from wealthy parents and classmates and membership in exclusive clubs.

So our current unequal society is not “the way it was meant to be” or some market-driven judgment on which of us are worthy of financial reward. Instead it is structured from the beginning to favor those who are already wealthy, in many cases through nothing but the luck to be born to the right parents.

This inequality is not inevitable. J.D. Vance noted that within two generations after his hillbilly family moved to Middletown, Ohio and got good jobs with Armco Steel “they had caught up to the native population in terms of income and poverty level.” Thoughtful and effective government policies can provide the needed thumb on the scale in favor of the working class to create jobs, income and a hopeful future. The cultural change and the connections will follow.